Tackling transparency: An examination of the state audit report of the Vineyard Redevelopment Agency

-

- Part of the new Utah City development is pictured Feb. 13, 2025, in Vineyard.

-

- Utah State Auditor Tina Cannon.

-

- Charts from the Utah State Auditor’s Office detail the alleged disparity of city funds between what was in Vineyard’s accounting system versus the updated figures uploaded to Transparent Utah.

-

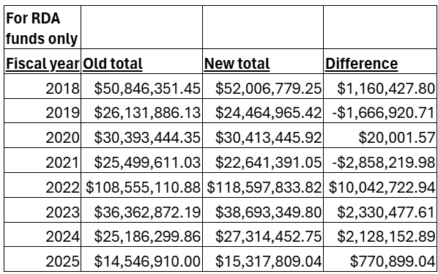

- Charts from the Utah State Auditor’s Office detail the alleged disparity of RDA funds between what was in Vineyard’s accounting system versus the updated figures uploaded to Transparent Utah.

The Office of the Utah State Auditor released its findings last week from the limited review audit it conducted of Vineyard City and its redevelopment agency.

The audit examined some of the entities’ financial transactions and contractual agreements and announced three findings of noncompliance or mismanagement. According to the audit:

- Vineyard did not properly report the use of its public funds to the state’s public financing website

- The city’s redevelopment agency operated without taxing entity committee involvement

- The city failed to disclose information related to property tax abatements.

Vineyard challenged the state auditor’s decision on several findings, requesting for some to be downgraded to an observation, but pledged to make adjustments to its reporting procedures and engagement with taxing entities.

Based on the details of the report and the response to the audit’s release, the two parties disagree on the severity of the findings.

Mayor Julie Fullmer said in a statement, “We are pleased that the State Auditor’s review found no evidence of misuse or mismanagement of public funds. We agree with the helpful Auditor’s recommendations, have already implemented them, and view them as a valuable opportunity to further strengthen our systems of transparency and public engagement.”

State Auditor Tina Cannon said Fullmer’s comments were at best, premature, and at worst, misleading, because the purpose of the audit was not to determine fraud or abuse but to determine what was spent. She added that Vineyard’s lack of transparency was “concerning.”

“The lack of trust in Vineyard is notable, and the solution to a lack of public trust is more transparency, not less. If you have nothing to hide, hide nothing and allow the public to see what you did,” Cannon said.

Vineyard City Manager Eric Ellis disagreed with the notion that the city is not transparent with its money.

“Vineyard takes financial transparency as seriously as we possibly can,” Ellis said. “We act in accordance with state laws, and in this particular situation, we welcome the audit and we welcome the findings. We made adjustments and tweaks as audits are intended to produce.”

Examining finding 1

The Utah State Auditor’s Office said it obtained Vineyard’s general ledger from 2018-2024 and found disparities in financial figures originally reported by Vineyard to Transparent Utah compared to what was found in the city’s accounting system.

According to the audit, some payments were entered into the accounting system after the file was uploaded to the state, with transactions omitted including substantial payments to developers from the RDA which could “raise public suspicions that those payments were intentionally hidden.”

The State Auditor’s Office shared numbers containing what was initially reported to Transparent Utah followed by what funds were reported in the city’s general ledger.

The largest disparity occurred in 2022, when the initial reported total was around $108.5 million to RDA funds and the new reported total was around $118.6 million, for a difference of $10,042,722.98. For the entire 2022 city budget, there was a disparity of around $17.5 million between the old and new total.

Cannon also tweeted the figures Friday, both for total funds and for RDA funds only, calling the RDA disparity “‘missing’ payments from the RDA to developers.”

Objecting to the tweet was former Vineyard City Manager Ezra Nair, now Utah County’s Administrator, who responded via X to say the chart did not show RDA payments to developers but actually showed total revenues and expenditures.

Nair told the Daily Herald on Tuesday the numbers Cannon presented regarding the RDA are “not accurate whatsoever.”

The RDA, according to Nair, has never generated over $100 million in expenses in a year, and he said the 2022 discrepancy of $10 million was due to revenue distribution at the end of the fiscal year, not due to payments from the RDA to developers.

“The accusation of high corruption on that front is just grossly misstated,” Nair said.

The State Auditor’s Office confirmed Tuesday that the figures show both revenues and expenses and said the current transaction total in Transparent Utah aligns with the accounting system of Vineyard.

Vineyard’s official response to the disparity was that payments were not intentionally omitted, but it was “unaware” quarterly transparency reports should be deleted and replaced with a comprehensive annual report when financial statements became finalized.

Ellis said the fiscal year ends on June 30, but the deadline to upload finances from the year’s final quarter is July 31, and the state is still delivering tax disbursements of sales tax and property tax in August. He said in 2022, there was $14.2 million that came in in August, and there was $3.3 million in debt services and depreciation expenses – but that it was not going to developers.

Vineyard referred to a May 22 audit alert sent to all local government entities in the state providing guidance on how to “post accounting and audit adjustments to revenue and expenditure data already uploaded to the Public Finance Website,” and said it was one of several cities that did not replace reports with full-year files if accruals or adjustments were posted to the accounting system after July 31.

“Our approach was we don’t have a solution for a deadline that the state has issued to us of July 31 and any transactions that happen after that,” Ellis said. “And once we had that solution, which was delete all your old reports and add a new, like, full year report, then we immediately did that. So it was simply an issue, a discrepancy between deadlines that the state had issued through transparent Utah and what we were reporting.”

The State Auditor’s Office countered that that the rule was “clearly established in both Utah statute and administrative code.” Cannon also argued that other cities making the same reporting mistake isn’t an excuse to make it yourself.

“If your friends are jumping off a cliff, you don’t jump off of it too,” she said.

Examining finding 2

The former Geneva Steel plant was acquired by Vineyard in the early 2000s, and the city established its own redevelopment agency, or RDA, in 2007 to clean up the site for development purposes.

The RDA is operated by the Vineyard City Council and receives Tax Increment Financing, or TIF, from different taxing entity committees, or TEC, including the Alpine School District, Central Utah Water Conservancy District and Utah County.

The auditor’s office found that the Vineyard RDA’s most recent project area budget approved by its tax entity committee was on Dec. 20, 2010, and that the TEC has not reconvened to review or approve action by the RDA, even though meeting on an annual basis was required.

“Failure to ensure all taxing entities actively participate creates public concerns about the legality of Vineyard’s Redevelopment Agency (RDA) actions,” the report read. “In addition, citizens are not able to obtain information regarding the use of funds from the government entity that levied the tax.”

Vineyard responded that once the TEC completed setting up the TIF by 2011, continuing to meet wasn’t necessary, and added that meeting annually was no longer a requirement, referring to SB70, which was 2011 state legislation that implemented an annual reporting requirement, instead of an annual TEC meeting.

However, the State Auditor’s office said in response to SB70, the city failed to change its own resolution which requires the annual TEC meeting to be held, meaning the annual meeting requirement remained in full effect.

Ellis said the city accepted the finding and said it’s taking steps towards getting the TEC to amend its bylaws.

“(That) is something that we’re going to have to work on, because people that were on the TEC originally are no longer in those positions,” he said. “And so we’re working with the taxing entities to gather an appointment for each of those entities, and then reconvene.”

The lack of oversight from the TEC for nearly 15 years was concerning to Cannon.

“Because there haven’t been meetings over what they’re doing and why they’re doing it and how they’re doing it; we can’t answer those questions,” she said. “There has not been disclosure of those types of things. Those are the very discussions and the answers that would be given in the meetings and the reports that are missing.

“You should be showing who those entities are, what the amount of money was … and where else it’s going.”

Ellis responded by sharing some figures. Since 2011, he said there’s been approximately $94 million in TIF going towards the Vineyard RDA, including $23 million toward environmental remediation, $22 million in developer infrastructure reimbursement and $40 million in bond payments.

The Utah City Development is a “major part” of the RDA, he said, and the city uses TIF funds to pay back “backbone infrastructure” for roads and water systems installed by developers.

Since development started on the Geneva site in 2011, Ellis said the value of the area has gone from $244 million to $1.7 billion.

“It’s a win for the city as those developers invest their dollars up front and are paid back as the value of the city goes up, and we’re able to pay for that with that tax increment,” Ellis said.

Examining finding 3

Vineyard’s failure to disclose tax abatement information, according to the audit report’s third finding, may lead to users misunderstanding the revenue forgone due to RDA agreements.

Vineyard’s response was that it had never entered into any tax abatement agreements.

The state auditor replied by providing the city with a definition and explained that the RDA, by its nature, has entered into many tax abatement agreements, because a tax abatement is an agreement where a government entity gives up tax revenue they’re entitled to and in exchange the entity promises to use the money for economic development.

“They just don’t seem to understand what (tax abatement) means,” Cannon said. “That is part of the problem. It’s a lack of transparency, and it’s a high level of a lack of transparency.

“In tax increments, the vast majority is from the school district. So anytime you are using school children’s money for things other than education, you should be very clear what you did instead, why you did it and how those children will benefit in the long term. … So that’s why it matters and why those reports are required.”

Ellis said the city did not understand the RDA had entered into tax abatement agreements, because the agreements were not called a “tax abatement,” but “reimbursements of tax increment for contracted work done.”

The solution, he said, is a “simple solution” to add footnotes to an annual report that describe the revenue and expenses completed for the year.

“It wasn’t a major issue,” Ellis said. “It was simply us explaining what our understanding of a tax abatement was versus what theirs was. And if they were calling our reimbursements tax abatements, totally fine; we added the footnotes that were needed to make sure that that request was satisfied.”

In an opening letter to the audit report, Cannon encouraged the city staff and officials to “set a tone” of civility. She said the best way to improve public trust is more transparency.

“If you have nothing to hide, hide nothing and allow the public to see what you did,” Cannon said.

Ellis said his message to the public is, “Vineyard is fully up to the task of being as transparent as it can be. We post updated records to the State Auditor’s site and to our own site. And really, if anyone has any interest in learning more about our financials, they can come in and look at them or put in a request, and we share those openly, and we’re grateful for the auditors report that helped us be just that much more transparent.”

Local News

Transforming the mall: Provo Towne Centre redevelopment plan goes through the legislative process

Utah aims to host critical minerals lab, hoping for federal recognition — and funding